-

The ESG Mindmap

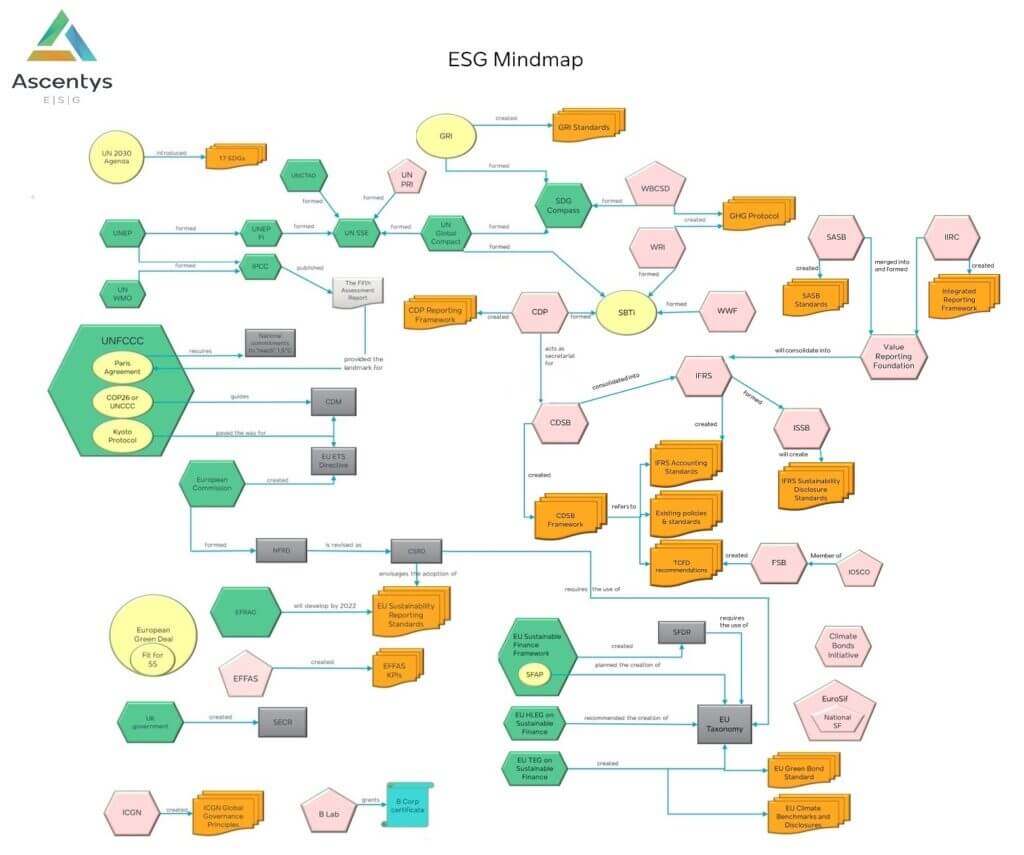

Ascentys ESG mindmap (c) A growing Ecosystem As sustainability & ESG are on their way to become mainstream, we see news of recent regulations, converging organizations,

-

ESG Glossary

B Corp: A B Corp is an organization that has successfully completed the certification put forth by the nonprofit B Labs. B Corps can only be for-profit organizations,

-

ESG: 21st century operational management tool

ESG is often linked to the Financial sphere, typically with reference to ESG ratings which are used to drive investment decisions. We are strong proponents of ESG as a modern

-

Earth day 2022

As sustainability & ESG are on their way to become mainstream, we see news of recent regulations, converging organizations, changing reporting standards every other day

-

ESG Policy Developments in the United States– March 2022

Environmental, social, and governance (ESG) policy has become prominent in recent years as the effects of climate change on the environment have revealed themselves

-

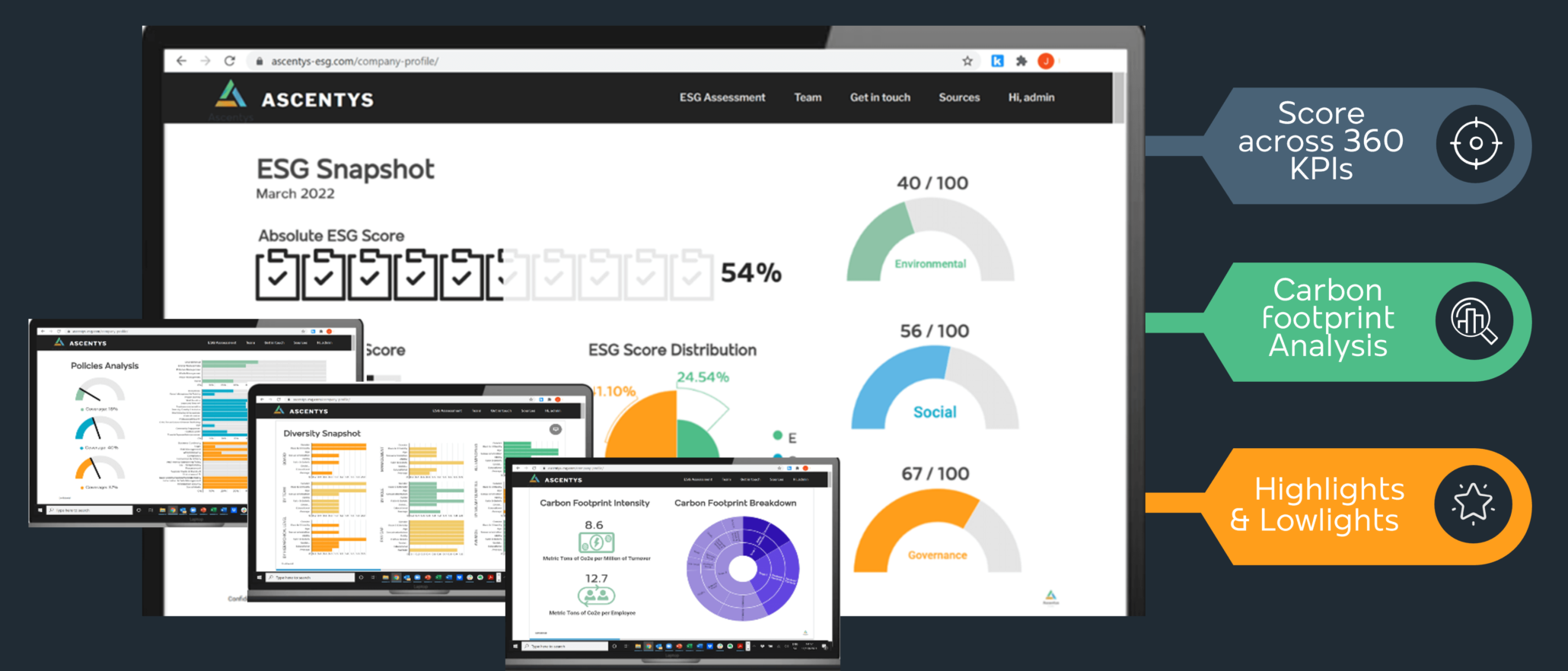

The “Non-Financial” performance management imperative. Are you ready?

Every company in the world, no matter its size, location or industry, monitors, measures, tracks, and to some extent reports on key Financial metrics…not just because it might be required